Largest Catering Companies Are Automating Away Their Own Workforce

The pitch was simple, and cities bought it every time. Build us a stadium, local officials were told, and we’ll bring jobs. We’ll bring foot traffic. We’ll bring economic life to this neighborhood. Taxpayers opened their wallets. Bonds were passed. Neighborhoods were rezoned. Families were displaced. And the stadiums got built — gleaming, massive, and full of promise.

Now, those same stadiums are being retrofitted with a new kind of promise. Not to the community. To the shareholder.

Artificial intelligence is remaking the inside of every major sports and entertainment venue in America — and quietly, methodically, it is doing exactly what every stadium promise never delivered on: redistributing wealth. Just not toward the communities that were sold the dream. The money is flowing upward, into the data centers of Cisco and IBM, into the earnings reports of Aramark and Compass Group, into the quarterly calls of venture-backed automation startups that have never once poured a beer in a stadium tunnel at 7 p.m. on a Sunday.

What follows is not a story about technology. It is a story about who pays, who profits, and who gets left standing outside the gates.

THE $43 BILLION PROMISE THAT WAS NEVER KEPT

According to the Citizens Against Government Waste, since 2000 state and local governments across the United States have spent $43.1 billion in public funds building professional sports stadiums. That figure does not include the additional $13 billion in new subsidy proposals the Tax Foundation reported across professional sports in a single year alone for new construction and renovations.

The economic case for these subsidies has always rested on a single argument: jobs. Construction jobs. Permanent operations jobs. The downstream economic activity of tens of thousands of fans flooding local businesses before and after games. The stadium as a jobs engine, a neighborhood anchor, a catalyst for revival.

Economists have spent decades testing that argument. Their verdict is nearly unanimous.

“The promised tangible economic benefits — economic growth, income growth, wage growth, employment growth, and higher tax revenues — do not occur the way that sports teams claim.” — Tax Foundation, 2024 literature review of 50 years of stadium construction

What stadiums actually generate, once built, are primarily part-time, seasonal, low-wage positions available in the NFL’s case for fewer than two weeks of actual game days per year. These event-day jobs — the cashiers, ticket-takers, concession runners, parking attendants, ushers, and security screeners — became the lived version of the economic promise. Not the good union jobs the brochures implied. But jobs nonetheless. Work that mattered to the people who held them.

In Cleveland, the public authority overseeing local stadiums owed MLB and NBA teams $25 million as of May 2024 for mandated repairs after dedicated tax revenues fell short of projections. The city — already carrying bond debt from 1990s stadium renovations — faced covering those costs from general fund revenues. The same fund that pays for police, fire, roads, and schools.

Charlotte’s $650 million stadium renovation commitment, according to a fiscal analysis cited by the Reason Foundation, exceeds the city’s entire annual municipal budget for police, fire, and solid waste services combined — a figure independently verifiable against Charlotte’s published FY2025 General Fund budget.

Source: Citizens Against Government Waste; Tax Foundation; Reason Foundation; Governing.com

ENTER THE ALGORITHM

Against this backdrop of broken promises and stretched municipal budgets, stadium operators have spent the past three years deploying a new generation of AI infrastructure. The investment case is straightforward: eliminate the labor cost of the very jobs the stadium was supposed to create.

Industry market forecasts estimate the global smart stadium market at roughly $11 billion in 2026 and is projected to reach $35 billion by 2034. The AI-in-sports market was valued at $9.8 billion in 2026 and is projected to hit $33.3 billion by 2031, growing at nearly 28 percent annually.

The companies collecting those revenues read like a who’s who of enterprise technology. Cisco, a leading infrastructure provider in smart stadium deployments worldwide, provides the networking backbone across dozens of major venues. IBM supplies AI analytics and has built an active sports tech startup ecosystem, running competitions in 2026 to identify and commercialize the next generation of automation tools. Amazon Web Services powers the NFL’s Digital Athlete simulation platform. Microsoft and Azure entered a multiyear AI partnership with the Mercedes-AMG F1 Team in January 2026. SAP and Oracle manage back-of-house operations and supply chain automation. Sportradar extended its exclusive data partnership with MLB through 2032, with the league taking an ownership stake in the company.

These are not fringe players experimenting with pilot programs. This is the permanent infrastructure of the modern stadium, and the documented effect has been the systematic removal of labor from the operating model.

Proof of the Pudding — an Atlanta-based catering company operating across PGA Tour events, Division I collegiate stadiums, and motorsports facilities — became the first foodservice operator to deploy Amazon’s Just Walk Out technology using RFID at a sports and events venue, debuting the system at Circuit of the Americas in October 2025. The new Nissan Stadium in Nashville, home of the Tennessee Titans, will run all concessions entirely on Just Walk Out technology. Amazon confirmed it has surpassed 70 deployments in sports and entertainment venues, with stadium operators moving from isolated pilots to full-scale adoption — describing the shift in their own words as venues going from testing Just Walk Out “in one or two sites” to declaring “this is proven technology.”

Source: Mordor Intelligence; Fortune Business Insights; Amazon; Retail TouchPoints

THE GIG WORKER IS THE FIRST DOMINO

To understand who loses first, you have to understand how stadiums are actually staffed. The vast majority of event-day workers are not employees of the team, the league, or even the venue. They are gig workers — hired per event through staffing agencies, concession management companies, and third-party vendors. They have no benefits, no guaranteed hours, and in most cases, no union protection.

These workers are not abstractions. They are the 19-year-old scanning tickets in Section 114. The 54-year-old working the beer stand because her restaurant job cut her shifts. The retired tradesman parking cars on Sundays. For many, stadium gig work stitches together a patchwork income alongside restaurant shifts, catering gigs, and other hospitality work in the same community.

That patchwork is being automated away, stitch by stitch.

At Cleveland Browns games, the team’s Express Access system — powered by Wicket’s facial authentication platform — processes tickets in two seconds on average, clearing entry gates ten minutes faster than traditional methods. The team reports saving over $8,000 per Wicket lane per season. Multiply that across a full stadium deployment, a full season, and an entire league, and the labor displacement math becomes significant.

Aramark, one of the largest foodservice operators in professional sports, deployed AI self-checkout technology across eight NFL stadiums during the 2025 football season. Its own public-facing technology documentation describes the goals of its concession automation program with unusual candor: to expand profits, boost customer satisfaction — and to “reduce staff in a tight market.”

Sodexo Live! posted organic growth of 23.4 percent in fiscal 2024, driven by what the company’s own earnings report described as “robust activity in all venues, and in particular strong per capita spend in sports stadiums.” The company’s CEO told investors it is embedding AI into core operations to “automate workflows and drive smarter data-driven strategies.” Compass Group’s leadership made similar commitments in parallel earnings calls.

Aramark’s own documentation names one of the three core goals of its AI concession rollout as reducing staff.

The algorithm does not hide what it is doing. Only the press release does.

The jobs being eliminated are not glamorous. But they were real. They were accessible to people with no college degree, no specialized skill set, and no connection to the technology industry. They were the jobs the stadium was actually built to support.

The scale of displacement is not hypothetical. It is a matter of arithmetic. A major NFL stadium employs between 1,500 and 2,500 event-day workers per game — cashiers, ticket scanners, concession runners, parking attendants, and guest services staff. Industry staffing data and Amazon’s own deployment figures indicate that between 40 and 60 percent of those roles are directly replaceable by currently deployed technology. At that rate, a single venue automation rollout eliminates between 600 and 1,500 shifts per event. Across a nine-game NFL home season, that is between 5,400 and 13,500 shift eliminations per stadium, per year — before a single concert, conference, or arena event is counted. Across all 32 NFL venues alone, the seasonal displacement calculation runs into the hundreds of thousands. Expand to MLB, NBA, MLS, and Division I college football, and the number of eliminated shifts reaches into the millions annually. These are not jobs that will be retrained into. They are jobs that will not be posted.

Source: Wicket; Aramark Sports + Entertainment; Sodexo FY24 earnings; Facilities Dive

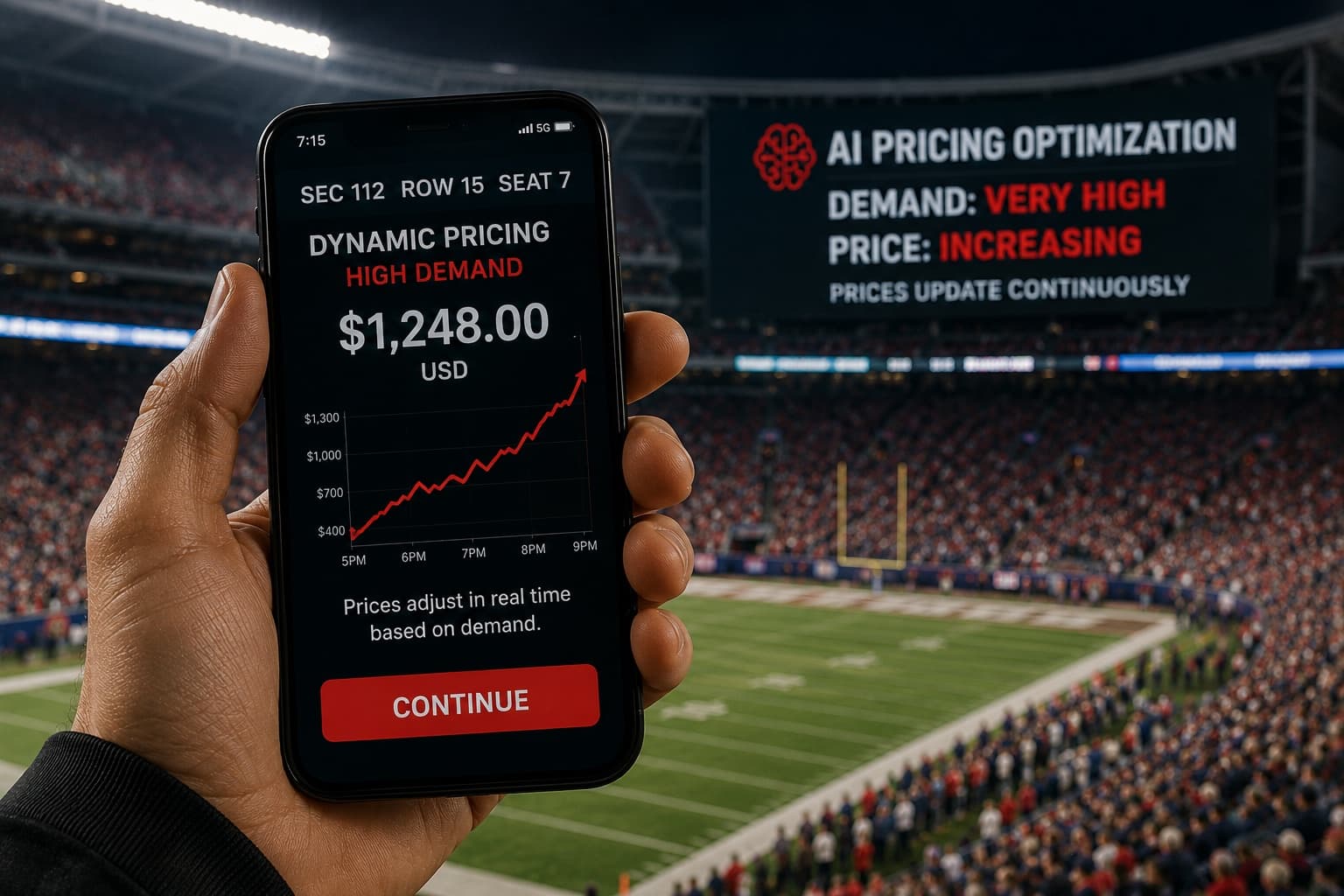

THE FAN PAYS MORE FOR LESS

While gig workers lose shifts, the consumer is being asked to pay more — significantly more — for the experience that automation was supposed to make seamless and affordable.

Dynamic AI pricing is now the standard operating model for major events. FIFA’s 2026 World Cup is the starkest example. The average ticket price for the tournament sits at approximately $563 — more than double the $253 average from Qatar 2022. Category 1 front-section seats for the US opener at SoFi Stadium were listed at $4,105 in late April 2026, up from $2,735 a week prior. The top ticket price for the World Cup Final reached $10,990 — with secondary market resale for the final expected to exceed $11,000 for the cheapest available seat.

This is not inflation. This is the architecture of AI-driven revenue maximization applied to the live experience, in real time, at scale. The system analyzes opponent quality, team performance, weather, day of the week, and social media sentiment. It reads the demand signals in search trends and adjusts prices upward at the precise moment fans are most likely to commit.

The broader trend confirms the pattern. According to CPI data, the cost of admission to concerts, theaters, and sporting events has risen approximately 26 percent since 2021. The average concert ticket price in 2025 hit $144, up 45 percent from $96 in 2019. Kansas City Chiefs season tickets now run $5,000 for fewer than ten home games.

AI ticketing vendors describe this capability with notable directness. TicketsOnline.AI’s 2026 implementation guide states the purpose is to enable venues to charge “the right amount at the right time to the right customer, maximizing both revenue and fan experience” — with documented revenue increases of 34 percent or more per deployment.

The fan, in other words, is not a beneficiary of AI in stadiums. The fan is the target.

Source: CNN; FIFA; CPI / BLS; TicketHold; TicketsOnline.AI

THE DOMINO FALLS OUTSIDE THE GATES

The impact does not stop at the stadium gates. It accelerates.

The same labor pool that once filled stadium shifts — concession workers, runners, prep staff — feeds directly into the broader restaurant economy. These are the entry points. The first jobs. The training ground for everything that follows.

When those jobs disappear, the pipeline breaks.

At the same time, restaurants across the United States are entering their own compression cycle. Full-service closures are rising. Fast-casual traffic is flattening. Independent operators are being squeezed between rising input costs and a customer base that is pulling back on discretionary spending.

The industry is not collapsing in a single event. It is being hollowed out from both ends.

Upstream, automation removes the lowest-cost labor. Downstream, cost pressure eliminates the operators who would have hired them.

The result is a structural gap. Fewer workers entering the system. Fewer businesses able to absorb them. More pressure on the operators who remain.

When AI concessions reduce friction at the point of sale — as AI self-checkout kiosks have done at Oracle Park, home of the San Francisco Giants, where Mashgin’s technology now processes transactions in under 19 seconds on average across more than 110 major league stadium deployments — fans spend more time in their seats and more money inside the venue. That is the explicit goal: capture the consumer dollar before it walks out the gate and down the street to the bar that has been serving pregame crowds for fifteen years.

Industry publications are describing this shift without apology. A 2026 AV Magazine forecast details how smart stadiums will connect every element of the surrounding entertainment district — hotels, bars, restaurants, clubs — back to the venue’s centralized experience and spend-capture infrastructure. The stadium is not just competing with local businesses. It is absorbing them into its economic orbit.

The independent restaurant near the stadium, which built its business model on the pregame rush and the halftime exodus, now faces a direct competitor with unlimited capital, AI-optimized pricing, mobile ordering infrastructure, facial-recognition payment lanes, and a product delivery system designed to eliminate the friction that used to drive people out of the venue.

Meanwhile, the same automation wave dismantling stadium labor is moving downstream into QSR and fast-casual restaurants with identical urgency. McDonald’s is expanding AI across its 2026 operations. White Castle has deployed Flippy, a robotic fry cook. Chipotle began testing automated makelines in 2025. Each of these moves signals the same structural shift: the entry-level food service job is being engineered out of the transaction layer across the entire industry, not just inside the stadium.

The gig workers displaced from stadium shifts do not retire. They circulate into the same local hospitality economy — the restaurants, catering companies, food trucks, and event venues that form the connective tissue of food service employment in any mid-size American city. As both ends compress simultaneously, the shared labor pool thins. Turnover rises. Scheduling pressure intensifies. The hospitality workers who remain face harder conditions for lower negotiating leverage.

Source: Mashgin; AV Magazine 2026; Restaurant Dive; Kiosk Industry

THE TRANSFER OF WEALTH, MEASURED IN REAL TERMS

It is worth stating clearly what is happening here, because the language of optimization tends to obscure it.

A community voted to tax itself, or its elected officials committed public funds, to build or renovate a sports facility. The justification was economic benefit to that community. The jobs, the foot traffic, the tax base, the neighborhood vitality — these were the promises made in exchange for public capital.

Those promises, by the near-unanimous consensus of economists studying five decades of data, were not kept. The jobs created were seasonal, part-time, and low-wage. The economic activity was largely substituted from elsewhere in the local economy rather than newly generated.

Now, the same facilities — in many cases still carrying public bond debt — are deploying automation that eliminates the low-wage seasonal jobs that were the one tangible form the economic promise actually took. The money saved on that labor does not return to the community. It flows to Aramark shareholders, to Cisco infrastructure contracts, to IBM analytics licensing, to Wicket — the facial-recognition ticketing company now processing entry at NFL and NBA venues nationwide. It flows, in the form of higher ticket prices extracted by AI dynamic pricing, directly out of the fan’s pocket and into the league’s revenue model.

The substitution effect that economists identified decades ago — the observation that stadium spending redirects consumer dollars rather than creating new ones — is now operating with algorithmic precision. AI is not just passively failing to generate new economic value for communities. It is actively extracting value that used to circulate locally, routing it to remote shareholders, and using dynamic pricing to increase the extraction rate in real time.

The stadium was sold to the community as an economic engine. The algorithm has turned it into an extraction machine.

This is not an argument against technology. It is an argument about accountability. When public money builds a facility, when a community bears the cost of that investment for thirty years, there is a legitimate question about who has the right to automate away the jobs that investment was supposed to create — and to whom the profits of that automation belong.

That question is not being asked in earnings calls. It is not being raised in city council chambers. It is not appearing in the press releases that announce the next AI concession rollout. It is, however, being felt on every game day by the person who shows up to find a kiosk where a colleague used to stand.

WHAT COMES NEXT

The pattern is already visible. The question is not whether it spreads. It is how fast.

In Russia, restaurant traffic has fallen to multi-decade lows, with closures rising under sustained cost pressure and weakening consumer demand. (Reuters; The Moscow Times)

In China, nearly 3 million food-service businesses closed in 2024 alone, even as large chains and delivery platforms expanded under tightening margins. (Reuters)

In Australia, hospitality has recorded some of the highest business closure rates across any sector, driven by rising costs and declining discretionary spending. (Restaurant & Catering Australia; The Guardian)

Different economies. Same outcome.

The removal of independent operators and the concentration of control into fewer, larger systems.

The United States is now entering the same phase. Restaurant closures are rising. Traffic is flattening. Costs remain elevated. At the same time, the lowest-cost labor layer is being systematically removed through automation — not just in stadiums, but across quick-service and fast-casual operations.

What emerges is not a collapse in the traditional sense. It is a compression. Fewer independent operators. Fewer entry-level jobs. Higher barriers to entry. Greater control concentrated in fewer hands.

The stadium is not an isolated case. It is an early indicator.

The same infrastructure — AI pricing, automation, centralized logistics — is now moving across the entire food economy. What happens inside the stadium does not stay inside the stadium.

It sets the model.

WHAT NEEDS TO HAPPEN

The investigative trail here is not hard to follow. Every stadium that has received public funding and is now deploying automation is a data point. Concessionaire contracts attached to publicly funded venue agreements may be subject to public records requests — and any that include language about labor reduction should be. Every bond agreement that promised community economic benefit is a legal document. Every city that is currently debating a new stadium subsidy is a decision point.

The accountability questions are specific: What are the labor terms in AI concession vendor contracts at publicly subsidized venues? Do existing community benefit agreements — many of which were written before AI automation was a realistic operational option — require renegotiation? Are dynamic AI pricing systems subject to any consumer protection oversight? Who owns the biometric and behavioral data collected by facial-recognition ticketing systems, and what are residents’ rights regarding that data?

Sports leagues and venue operators are not obligated to prioritize community welfare over shareholder return. That is a structural reality, not a moral failing. But cities and states that continue to extend public subsidies to facilities deploying automation against the communities those subsidies were meant to serve are making an active choice. So are the concessionaire giants whose logistics depend on publicly funded infrastructure, publicly trained workers, and publicly maintained roads — while posting quarterly earnings growth alongside documented workforce automation investments.

The domino effect is not a metaphor. It is a sequence of documented economic decisions with traceable consequences.

The consequences are already happening. The only question is who is positioned to benefit from them.

Related Articles on IMFounder

- How Sysco Corporation Consolidated the Middle Layer of Food Distribution

- 7 Shocking Reasons Trees Are the Rarest Resource on Earth — And We’re Erasing Them Fast

- Hair Fall & Shower Water: Causes, Prevention, and Technology — Hard Water, Hair Loss, Prevention Tips & Best Shower Filters Explained

- Most Popular Holiday Drinks in North America — including hot chocolate, mulled wine, peppermint mocha, and eggnog

- Best Places for Stunning Fall Foliage — Top Road Trips & Hidden Gems for Peak Fall Colors in North America

- The Rise of Streetwear in North America: From Subculture to Mainstream — Culture, Brands & Future

{kind=link}