The GLP-1 food industry disruption may become one of the biggest shifts in consumer spending over the next decade. The global food economy was built on a remarkably stable assumption:

Consumers would continue wanting more.

More appetizers. More alcohol. More snacks. More desserts. More late-night delivery. More convenience. More consumption.

For decades, the restaurant and packaged-food industries engineered business models around behavioral appetite expansion. Hospitality operators optimized menus around attachment sales. Beverage companies built empires around habitual consumption. Stadiums, airports, casinos, and entertainment venues relied on impulse purchases at extreme markups to subsidize operating margins.

Then pharmaceutical companies introduced a class of drugs designed to suppress appetite itself.

What began as a diabetes and obesity treatment is rapidly becoming a structural economic force.

Medications such as Ozempic, Wegovy, and Mounjaro are beginning to alter food purchasing behavior, restaurant traffic patterns, alcohol consumption, and discretionary spending across multiple sectors simultaneously.

Morgan Stanley projects the global GLP-1 market could reach $190 billion by 2035. JPMorgan estimates GLP-1 adoption could remove between $30 billion and $55 billion annually from food-and-beverage industry sales by 2030. By the end of 2024, Ozempic, Rybelsus, and Wegovy had already generated approximately $71 billion in cumulative US revenue — with projections showing the five leading GLP-1 drugs reaching $470 billion in cumulative US revenue by 2030.

The implications are no longer theoretical.

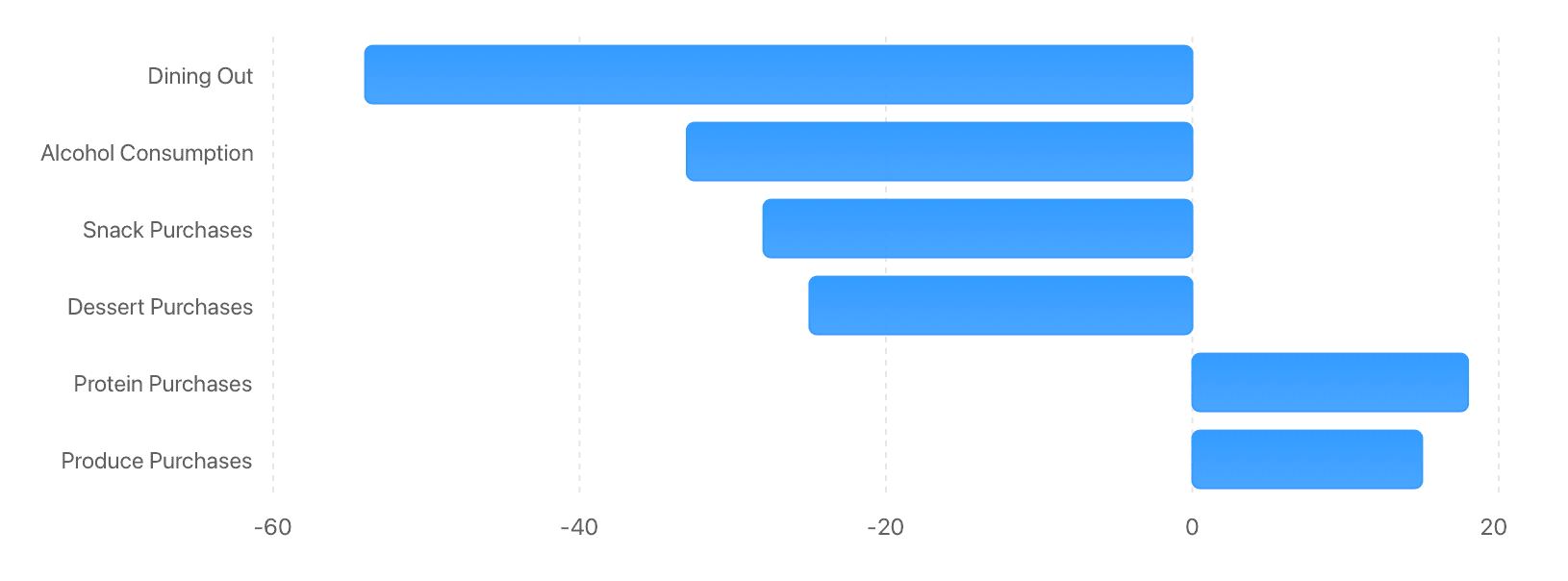

According to Circana research, GLP-1 users are purchasing fewer snacks, ordering fewer side dishes, reducing dessert purchases, consuming smaller portions, shifting toward protein-heavy foods and produce, and spending less overall on food.

Additional consumer surveys found 54 percent of GLP-1 users reported dining out less or significantly less after beginning the medication.

The Consumption Shift Behind GLP-1 Adoption

Consumer Behavior Changes Among GLP-1 Users

Research shows GLP-1 users are reducing discretionary food and beverage consumption while increasing healthier food choices.

For the restaurant industry, that distinction matters enormously.

The profit structure inside hospitality has never been distributed evenly across the menu. High-margin categories such as alcohol, appetizers, desserts, and impulse add-ons frequently subsidize the economics of the entrée itself.

A cocktail may carry a product cost between 12 and 18 percent. Desserts frequently operate below 25 percent food cost. Soft drinks can exceed 1,000 percent markup. Alcohol remains one of the most profitable categories in hospitality.

GLP-1 medications directly interfere with those attachment-sale behaviors.

A guest skipping a second drink, splitting an entrée, or declining dessert may appear insignificant in isolation. Across thousands of transactions, however, the cumulative impact becomes structural.

Operators are beginning to see the effects quietly: smaller checks, weaker alcohol sales, slower dessert movement, reduced snack purchases, and softer late-night traffic.

Source: Morgan Stanley GLP-1 market projection; JPMorgan February 2026; I-MAK GLP-1 revenue analysis 2025; Circana November 2025

How GLP-1 Drugs Are Affecting Alcohol Sales

The pressure is appearing globally.

According to IWSR, global beverage alcohol volume declined 2 percent in 2025 across markets representing approximately 75 percent of worldwide alcohol consumption. In the United States, beer volume declined 6 percent, wine fell 6 percent, and spirits dropped 4 percent.

Global wine consumption fell to its lowest level since 1957. French wine and spirits exports declined 8 percent. Exports to the United States dropped 21 percent. Cognac exports fell 24 percent.

At the same time, generational drinking behavior is changing rapidly. Gallup found the percentage of Americans who report consuming alcohol fell from 62 percent to 54 percent in just two years. Deloitte research found 65 percent of Gen Z consumers planned to reduce alcohol consumption further in 2025.

GLP-1 users are accelerating that trend. PwC research found 33 percent of habitual heavy drinkers reduced alcohol consumption after beginning GLP-1 medications.

That creates a significant problem for hospitality because beverage sales frequently subsidize labor, occupancy costs, and operational overhead.

The disruption extends beyond restaurants. Stadiums, airports, casinos, cruise operators, and entertainment venues rely heavily on high-margin convenience spending — beer, cocktails, snacks, desserts, and impulse purchases inside captive environments. A consumer purchasing fewer alcoholic beverages or skipping concession purchases has an outsized impact on profitability throughout the broader experience economy.

Source: IWSR Global Beverage Alcohol Report 2025; Gallup 2025; Deloitte Gen Z consumer research 2025; PwC The Business of Losing Weight 2025

The K-Shaped Food Economy

At the same time, the global consumer economy is increasingly splitting into two distinct groups.

The New York Fed reports recent consumer spending growth is being driven disproportionately by households earning more than $125,000 annually, while lower-income consumers continue reducing discretionary spending.

This is producing what economists increasingly describe as a K-shaped economy.

At the top: private chefs, luxury wellness retreats, high-protein meal systems, functional beverages, personalized nutrition, and premium hospitality experiences continue growing.

At the bottom: consumers are reducing restaurant visits, buying cheaper groceries, cooking at home more frequently, and eliminating discretionary purchases altogether.

The middle absorbs the pressure. Casual dining chains. Neighborhood bar tabs. Mid-tier hospitality concepts dependent on discretionary spending. The apps-and-drinks economy that dominated post-2000 dining culture.

The wealthy are still spending. They are simply consuming differently: fewer calories, less alcohol, more wellness, more protein, more optimization, and fewer impulse indulgences.

Source: New York Fed Consumer Spending Data 2026; Black Box Intelligence 2025; McKinsey State of Food and Beverage April 2026

The Industry Is Responding — to the Wrong Problem

The food industry has already begun adapting. Nestlé recently launched GLP-1-focused food products designed specifically for appetite-suppressed consumers. Major food manufacturers are increasing investment in protein-heavy, fiber-focused, and satiety-oriented product lines.

The same industry that spent decades engineering hyperpalatable products optimized for overconsumption is now racing to develop products compatible with appetite suppression.

That contradiction captures the broader transition underway.

The modern food economy was engineered around a highly reliable human behavior: the desire for excess. Not survival hunger. Commercial appetite. The second drink. The dessert. The snack. The impulse order. The late-night delivery notification arriving at precisely the right psychological moment.

That system became one of the most profitable consumption models in modern economic history.

Now pharmaceutical science is beginning to suppress the neurological mechanism underneath it.

Novo Nordisk has filed 320 patent applications on the molecule doing the suppressing. 154 have been granted. 49 follow-on patents extend protection to 2042. The company is not selling appetite suppression as a product. It is selling it as infrastructure. And unlike a restaurant concept that can be repositioned or a product line that can be reformulated, a patent thicket extending to 2042 does not pivot.

It compounds.

Source: I-MAK patent analysis 2025; PharmaVoice April 2025; Novo Nordisk SEC filings Q1 2026

The Bottom Line

GLP-1 adoption alone is not responsible for weakening hospitality traffic, declining alcohol sales, or changing consumer behavior. Inflation, debt, housing costs, fuel prices, and economic uncertainty are all contributing pressures.

But GLP-1 medications are accelerating shifts already underway across the global hospitality economy.

And if appetite itself becomes medically suppressible at scale, the restaurant industry may be forced to confront a structural reality it has spent decades avoiding.

The modern food economy was never built simply to feed people.

It was built to monetize craving.

Related Articles on IMFounder

- How Sysco Corporation Consolidated the Middle Layer of Food Distribution

- How Big Tech Is Quietly Taking Control of the Food Supply

- The Restaurant Industry: The Fastest Way Into the Economy Is Closing

Sources: Morgan Stanley GLP-1 market projection; JPMorgan Global Research February 2026; I-MAK GLP-1 Patent and Revenue Analysis 2025; Circana November 2025; IWSR Global Beverage Alcohol Report 2025; Gallup 2025; Deloitte Gen Z consumer research 2025; PwC The Business of Losing Weight 2025; New York Fed Consumer Spending Data 2026; Black Box Intelligence 2025; McKinsey State of Food and Beverage April 2026; Nestlé investor communications 2025; Novo Nordisk SEC filings Q1 2026; PharmaVoice April 2025

{kind=link}